Word: The next is the testimony of Daniel Bunn, President and CEO on the Tax Basis, ready for a Senate Finance Committee listening to on Might 11, 2023, titled, “Cross-border Rx: Pharmaceutical Producers and U.S. Worldwide Tax Coverage.”

Chairman Wyden, Rating Member Crapo, and distinguished members of the Senate Finance Committee, thanks for the chance to offer testimony on the worldwide tax system. I’m Daniel Bunn, President & CEO of Tax Basis.

I’m going to cowl three subjects in my testimony at the moment. First, I’ll share my views on the motivations and results of the reforms launched by the Tax Cuts and Jobs Act (TCJA). Second, I’ll focus on how present ranges of tax uncertainty undermine the targets of those reforms and the way that uncertainty is linked to the worldwide minimal tax. Lastly, I’ll discuss a strategic strategy to altering U.S. cross-border tax guidelines.

Worldwide tax guidelines within the U.S. have been overhauled as a part of the Tax Cuts and Jobs Act in 2017. The modifications shifted how U.S. corporations structured their investments overseas and led to some onshoring of mental property (IP).

In 2021, greater than 130 nations agreed to a top level view for worldwide tax reform. That define described formidable proposals to alter the taxation of huge multinational companies with a shift of their tax base towards market nations alongside a world minimal tax. The 2 items, referred to as Pillar One (the shift within the tax base) and Pillar Two (the worldwide minimal tax), will impression the way in which massive companies organize their tax affairs and the way in which governments design their tax insurance policies.

This 12 months, greater than two dozen nations are anticipated to place the worldwide minimal tax guidelines in place, and U.S. tax guidelines are on a collision course with these international guidelines. That’s as a result of U.S. tax guidelines adopted in each the TCJA and the Inflation Discount Act (IRA) differ considerably from the worldwide minimal tax guidelines.

Slightly than supporting a real secure harbor for U.S. guidelines, the U.S. Treasury Division has negotiated a deal that exposes the U.S. tax base in critical methods. Congressional motion is required to restrict U.S. corporations’ publicity to a number of layers of taxation and compliance that may hinder their capacity to compete on a world scale.

Evaluating the TCJA Worldwide Guidelines

The TCJA reforms weren’t good, however they moved the U.S. in the precise course.

It’s useful to think about why an organization would possibly need to make investments abroad or the way it would possibly need to interact overseas clients. An organization might be able to increase its U.S. operations and attain overseas customers both digitally or by way of the worldwide buying and selling of products. An organization might also decide that the easiest way to achieve overseas clients is by organising manufacturing services in places nearer to its clients. Abroad hiring and funding on this case wouldn’t be offshoring; it will be obligatory to achieve overseas customers. Lastly, an organization could use a 3rd nation as a base for reaching customers in a number of jurisdictions. This might be attributable to native pure sources, related analysis services and laboratories, or different elements.

Taxes may also play a job in these selections.

Cross-border tax coverage must steadiness at the least three targets. The primary must be to help home corporations of their home and abroad expansions as they search to achieve clients, supply supplies, and experience from around the globe. The second must be to help funding from overseas corporations into the home market. And the third goal must be to attain the primary two whereas additionally defending the home company tax base.

The TCJA tried to perform all three.

When it comes to the primary goal, the TCJA included three main insurance policies to help funding by U.S. corporations: reforms to headline tax charges, worldwide guidelines, and the therapy of capital expenditures.

Previous to the TCJA, the U.S. operated a worldwide tax system with the choice to defer taxes on overseas revenue till the earnings have been repatriated, an strategy most developed nations had deserted in favor of a territorial tax system that largely exempts overseas earnings from home tax.[3] To make issues worse, when U.S. corporations introduced earnings again, they confronted a federal tax charge of 35 %, which was the best company tax charge within the Organisation for Co-operation and Improvement (OECD).

The TCJA changed this with a extra aggressive 21 % charge, which, mixed with state-level company taxes, put the U.S. mixed charge at 25.81 %. In 2022, this was simply above the common of 23.57 % amongst nations within the OECD and the worldwide common of 23.37 %.[4]

The company tax charge discount was paired with the introduction of a dividends acquired deduction, a function widespread to territorial tax methods.[5] The dividends acquired deductions implies that overseas earnings might be introduced again to U.S. shareholders with out an extra layer of U.S. tax—the previous repatriation tax was eradicated.

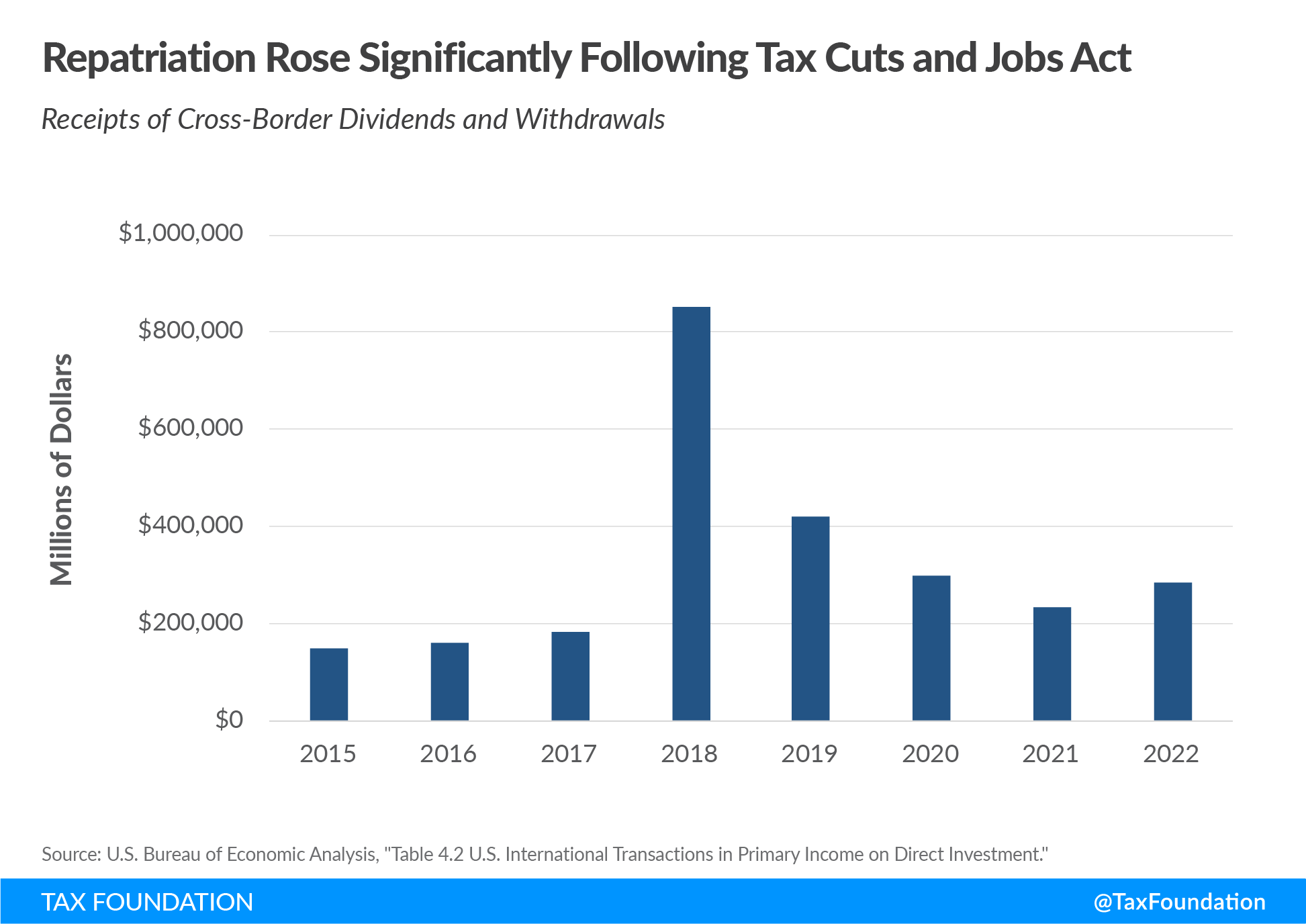

Within the 5 years instantly following the passage of the TCJA (2018-2022), corporations repatriated $2.1 trillion in overseas earnings. That may be a dramatic enhance relative to the 5 years main as much as tax reform (2013-2017), when corporations repatriated simply $797 billion.[6]

simply 2021 and 2022 versus 2016 and 2017, repatriations are averaging 0.04 share factors larger as a share of gross home product. That’s practically $43 billion in extra repatriated earnings annually obtainable to U.S. corporations that wish to put money into manufacturing and their workforce or return money to shareholders.

A working paper from educational accountant Brooke Beyer and his coauthors on the utilization of repatriated {dollars} has discovered that U.S. multinationals with low home liquidity and excessive home funding alternatives responded to the TCJA modifications with extra home capital expenditures.[7] On this method, alternatives for getting items and companies to customers have been mixed with a decrease U.S. tax burden to help funding within the U.S.

Along with the company charge discount and the dividends acquired deduction, the TCJA launched the coverage of speedy expensing for a big portion of capital investments (gear and different short-lived belongings) which is now expiring.[8] The modifications to the company tax charge and the adoption of speedy expensing had the impact of reducing the marginal tax charge on home funding, bettering incentives for enterprise funding.[9]

These insurance policies have been additionally helpful by way of the second goal, turning into a lovely funding vacation spot for overseas corporations.

A working paper by economist Thornton Matheson and her coauthors finds inbound overseas direct funding financed out of retained earnings elevated following the adoption of the TCJA.[10]

Trying on the third goal for cross-border tax guidelines brings one to the alphabet soup of the TCJA. In making an attempt to attain the targets of overseas success of home corporations and home success of each overseas and home corporations whereas defending the U.S. tax base, the TCJA introduced in two minimal taxes and one diminished tax charge.

The primary international minimal tax was adopted by the U.S. as a part of the TCJA. The coverage, the tax on World Intangible Low-Taxed Earnings (GILTI), was paired with an incentive for holding IP inside the U.S. (the Overseas-Derived Intangible Earnings [FDII]), and a disincentive for cross-border price shifting (the Base Erosion and Anti-Abuse Tax [BEAT]). [11]

These reforms broadened the U.S. tax base in a number of methods.

GILTI expanded the scope of U.S. corporations’ overseas income that face extra tax by the U.S. on an annual foundation. Previous to the TCJA, corporations might defer U.S. tax legal responsibility on their overseas earnings till the earnings have been repatriated. Following the TCJA, overseas income above a ten % return on belongings face at the least a ten.5 % minimal tax charge from GILTI, and overseas earnings will be repatriated with out an extra toll tax.[12]

In lots of circumstances, the tax charge corporations face beneath GILTI is 13.125 % or larger. The upper charge is as a result of overseas tax credit are restricted to 80 % of their worth and a few home bills are allotted to overseas earnings. The mixed tax (overseas taxes plus U.S. taxes) on the U.S. share of overseas income, lately estimated by Tax Basis economist Cody Kallen, was 19.3 % beneath present legislation for 2022.[13] Beneath present legislation in 2031, the mixed tax on overseas income of U.S. corporations would rise to twenty.7 %. That is primarily as a result of the tax charge on GILTI is scheduled to rise after 2025.

By design, GILTI has modified the incentives for investing in overseas low-tax jurisdictions as a result of the ground for overseas tax charges is not zero.

A working paper by economist Matthias Dunker and his coauthors examines how GILTI impacted incentives for corporations to amass companies in overseas low-tax jurisdictions. In comparison with corporations not impacted by GILTI, they discover that GILTI-affected corporations have been much less prone to merge with or purchase overseas corporations in low-tax places. Their analysis additionally reveals that acquisition targets for U.S. corporations impacted by GILTI are typically much less worthwhile.[14] Equally, analysis by educational accountants Harald Amberger and Leslie A. Robinson suggests the TCJA reforms diminished the quantity of tax-motivated cross-border acquisitions by U.S. corporations.[15]

Corporations dealing with extra tax by GILTI might make overseas investments to attenuate their GILTI publicity as a result of exclusion of a ten % return on certified enterprise asset funding (QBAI).[16] Beforehand talked about analysis from educational accountant Brooke Beyer and coauthors means that GILTI led to a rise in overseas capital expenditures.[17]

The subsequent method TCJA broadened the tax base was by way of FDII, which was designed to offer a decrease tax charge of 13.125 % on income from exports associated to IP held inside the U.S. The purpose of the decrease tax charge was to incentivize companies to maintain their software program, patents, or copyrights within the U.S. relatively than offshoring them to a overseas low-tax jurisdiction. In some circumstances, companies have returned IP belongings to the U.S. lately.

When IP belongings are held offshore, the U.S. tax base solely advantages to the extent that GILTI or different guidelines addressing tax avoidance apply. When IP belongings are within the U.S., the IRS has the first proper to tax associated earnings.

Analysis targeted on firm monetary statements has recognized U.S. corporations that particularly benefited from FDII as a result of they restructured their IP holdings.[18] Moreover, latest analysis by economist Javier Garcia-Bernardo and his coauthors reveals the driving drive behind a discount within the share of income that U.S. corporations e-book overseas was repatriations of IP.[19]

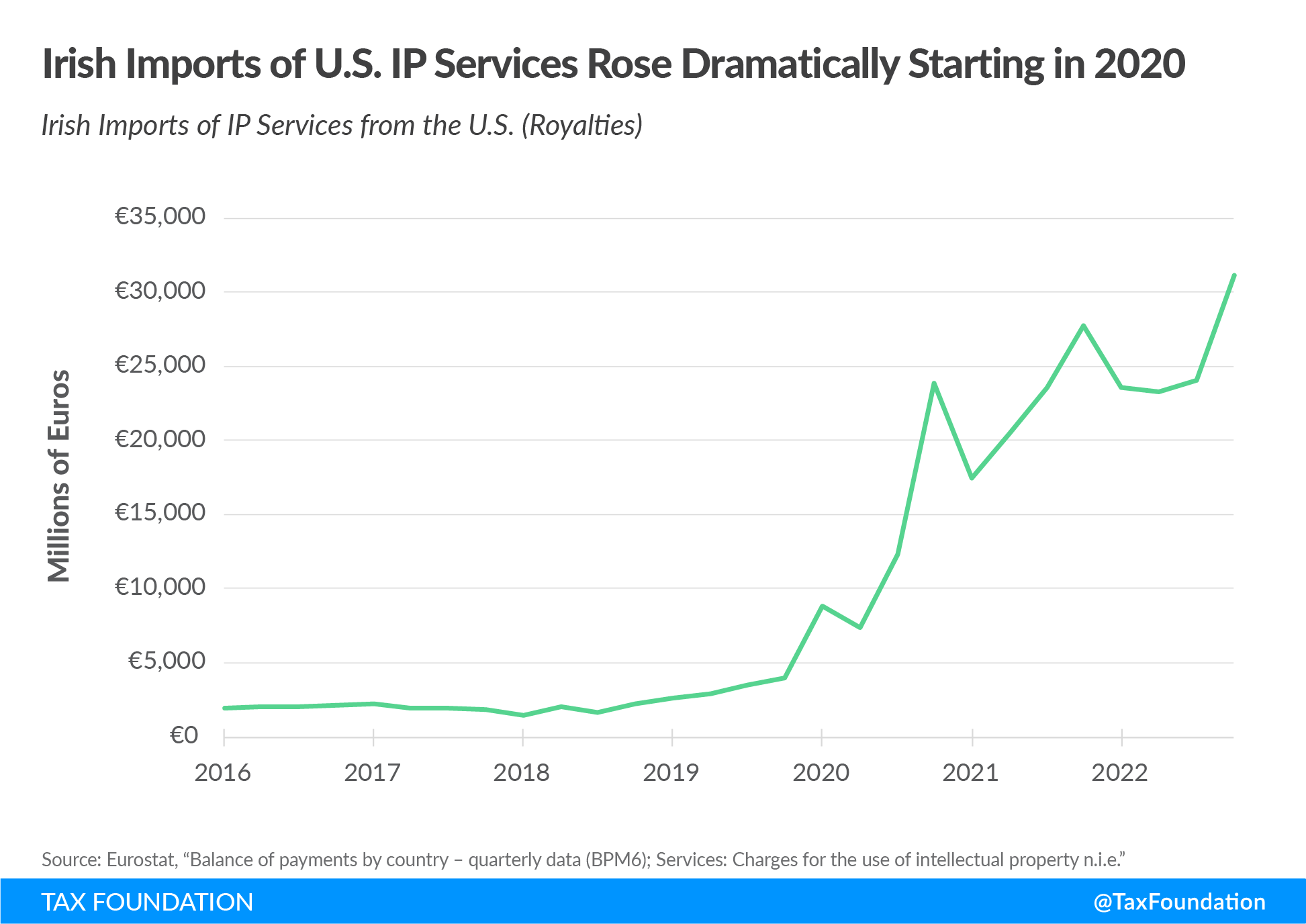

One attention-grabbing indicator of that is exports of IP companies to overseas jurisdictions, notably to Eire. For tax causes, many U.S. corporations have deployed investments in Eire as a part of their company constructions and funding methods in latest many years. Previous to 2020, additionally they usually used entities within the Netherlands and zero-tax jurisdictions to attenuate the quantity of taxes paid on income from IP.[20]

Nonetheless, since 2020—the 12 months many Irish constructions turned unavailable to corporations—such methods have been not viable.[21] Consequently, many U.S. corporations introduced IP again to the U.S. to serve Irish (and different) markets with IP held within the U.S. Because the begin of 2020, U.S. exports of IP companies to Eire have skyrocketed.

From the beginning of 2020 to the top of 2022, Irish entities had imported €243.8 billion ($267.9 billion) in IP companies from the U.S.—greater than triple the IP companies imports within the earlier decade.

A lot of the IP that has been shifted again to the U.S. has come from offshore monetary facilities akin to Bermuda and the Cayman Islands.[22]

The subsequent growth of the U.S. tax base is the BEAT. Just like the tax on GILTI, the BEAT is a minimal tax. It’s meant to handle tax-planning schemes the place massive multinationals make cross-border funds inside their companies to restrict their publicity to U.S. taxes. Since outbound funds are sometimes deductible within the U.S., and the “revenue” to a overseas subsidiary could also be taxed extra flippantly, such funds have been recognized to “strip” in any other case taxable revenue out of the U.S. into low-tax jurisdictions. The BEAT charge is 10 % and applies to corporations with greater than $500 million in complete revenues and complete cross-border funds that exceed 3 % (2 % for some monetary corporations) of deductions.[23]

GILTI, FDII, and BEAT are imperfect. The burden of GILTI and its interplay with overseas tax credit score guidelines means it operates extra like a surtax than a minimal tax. The BEAT is an inelegant strategy to addressing tax avoidance by way of cross-border shifting. Like several different tax measure, it could erode tax incentives. FDII additionally was not good, however its imperfections are extra in regards to the coverage narrative adopted by the present administration relatively than issues with the coverage itself. Particularly, the Biden administration has proposed to remove FDII and change it with unspecified analysis and growth (R&D) incentives.[24]

With home funding, inbound funding, and shifts in IP holdings linked to the TCJA modifications, it’s clear that these modifications have been in the precise course, even with their imperfections.

Analysis targeted on the change in enterprise tax burdens after tax reform has discovered that home revenue acquired a considerably bigger tax reduce than overseas revenue. The discovering isn’t a surprise for the reason that company tax charge was diminished so considerably, and the tax reduce acquired by multinational corporations was pushed by the change of their home tax legal responsibility. The tax burden on overseas earnings didn’t change considerably. Even after accounting for the change to the brand new cross-border guidelines, the overseas actions of U.S. multinationals face comparable ranges of tax in comparison with the earlier system.[25]

One last level of proof is how the TCJA modified the competitiveness of U.S. multinationals. Main as much as the passage of the TCJA, Bloomberg documented dozens of U.S. corporations that moved their headquarters exterior the U.S. between 1982 and 2017.[26] Since tax reform, this has primarily stopped.[27] It’s secure to say that relative to U.S. tax guidelines in place earlier than the 2017 reform, U.S.-headquartered corporations are rather more aggressive with their international friends.

Transferring into the Fog

The targets of the Tax Cuts and Jobs Act are actually being undermined by a local weather of uncertainty surrounding U.S. tax guidelines. The adoption of worldwide minimal tax guidelines around the globe, the administration’s proposal to repeal FDII, and upcoming charge modifications to GILTI and BEAT after 2025 within the context of doubtless unstable political coalitions all spell a recipe for uncertainty.[28]

Certainty and stability are exhausting to measure, however they’re sturdy contributors to a aggressive coverage surroundings.

Uncertainty stems first from the worldwide minimal tax guidelines. These guidelines don’t match up with U.S. tax guidelines or ideas, and plenty of U.S. corporations are at present getting ready to adjust to one more layer of minimal taxes regardless that Congress has not acted.

There’s additionally uncertainty in regards to the legality and enforceability of the worldwide minimal tax guidelines. Any coverage harmonization mission involving dozens of jurisdictions and their very own nationwide authorized frameworks will run into challenges, and the worldwide minimal tax isn’t any completely different.

Uncertainty additionally exists for congressional lawmakers making an attempt to chart the proper coverage course.

Within the fall of 2021, the Construct Again Higher Act (BBBA) handed by the Home of Representatives. The bundle included modifications to GILTI, FDII, and BEAT. Among the proposals would have improved the way in which the insurance policies work relative to present legislation, primarily the GILTI provisions that will restrict the quantity of home bills allotted to overseas income.

A serious problem for legislators on the time was that the mannequin guidelines for the worldwide minimal tax had not but been launched. If U.S. legislators had the mannequin guidelines in hand when designing the provisions of the BBBA, it’s probably they’d have made completely different selections.

The mannequin guidelines for the worldwide minimal tax have been launched in December 2021.[29] Additional commentary and examples of how the principles would possibly apply have been launched in March 2022, and administrative steering was launched in February 2023.[30]

Key variations between the mannequin guidelines and the executive steering have elevated the necessity for Congress to behave to keep away from a chaotic end result for U.S. corporations within the coming years.

However with out coordination between Congress and the U.S. Treasury Division, lawmakers could proceed to be unsure about applicable modifications that may shield the U.S. tax base and keep U.S. competitiveness.

The worldwide minimal tax establishes a 15 % efficient tax charge based mostly on the adjusted monetary assertion revenue of huge company entities on a jurisdiction-by-jurisdiction foundation. Beneath the minimal tax, an organization would want to calculate the efficient tax charge its operations face in every jurisdiction the place it has ample income. After accounting for regular company revenue taxes, a top-up could also be assessed to make sure the efficient tax charge in a jurisdiction is 15 %. A substance-based revenue exclusion is supplied each for a share of tangible belongings and payroll.

The foundations additionally use a world income threshold of €750 million ($790 million) in at the least two of the earlier 4 fiscal years with an elective exclusion for entities in a jurisdiction with common revenues under €10 million ($10.55 million) or revenue lower than €1 million ($1.05 million) (the common is calculated utilizing the present 12 months and two earlier years). The thresholds decide whether or not an organization must adjust to the principles generally or in a particular jurisdiction.[31]

The foundations lay out 4 instruments for implementing top-up taxes on low-taxed revenue. Typically, the primary three guidelines apply to the identical definition of taxable revenue, however they differ wherein jurisdiction would possibly apply the rule and the place a multinational would possibly ship its tax cost for the top-up.

The three most important guidelines of the worldwide minimal tax are as follows:

- Certified Home Minimal High-Up Tax (QDMTT): Applies to low-tax income inside a jurisdiction’s personal borders

- Earnings Inclusion Rule (IIR): Applies to low-tax income of overseas subsidiaries of a jurisdiction’s personal corporations

- Beneath-Taxed Income Rule (UTPR): Applies to a neighborhood subsidiary of a overseas firm that has low-tax income elsewhere on the earth that aren’t taxed beneath the opposite top-up guidelines; a guardian firm’s low-tax revenue might be allotted by formulation to a overseas jurisdiction for the aim of a top-up tax on a neighborhood subsidiary

A fourth rule based mostly on tax treaties is the Topic to Tax Rule (STTR), which a rustic might use to use a 9 % tax on funds to associated events taxed under that charge.

Additionally, the three most important guidelines of the worldwide minimal tax solely roughly correspond to proposals within the BBBA handed by the Home of Representatives in 2021. For instance, the proposed modifications to GILTI wouldn’t match the tax base of the minimal tax guidelines as they don’t use monetary accounting. The substance-based revenue exclusion would solely apply to tangible belongings relatively than payroll. Moreover, the efficient tax charge calculation for GILTI features a restrict on overseas taxes paid (95 % within the BBBA; present legislation solely offers an 80 % credit score). The per-country efficient charge might be 15.8 % or larger beneath the BBBA model of GILTI.

The variations, alongside the complexities of U.S. overseas tax credit score guidelines, create important gaps between the BBBA and the worldwide minimal tax mannequin guidelines.

Moreover, the e-book minimal tax adopted within the Inflation Discount Act in 2022 introduces one other definition of adjusted monetary assertion revenue that differs from the worldwide minimal tax guidelines.

Desk 1 offers a comparability of the completely different guidelines and the way they’re distinct from each other.

| Present Regulation | Scheduled Change to Present Regulation | Inflation Discount Act E-book Minimal Tax | Construct Again Higher Act (Not Adopted) | World Minimal Tax Mannequin Guidelines | |

|---|---|---|---|---|---|

| Efficient Date | 1/1/2018 | 1/1/2026 | 1/1/2023 | 1/1/2023 | 2023 (12/31/2023 for the EU and UK) |

| Price | 10.5% (might be 13.125% or larger relying on publicity to overseas taxes) | 13.125% (might be 16.4% or larger relying on publicity to overseas taxes) | 15% | 15% (might be 15.8% or larger relying on publicity to overseas taxes) | 15% |

| Exclusion for a Regular Return on Tangible Property | 10% deduction for overseas tangible belongings | 10% deduction for overseas tangible belongings | Tax accounting is used for depreciation deductions | 5% deduction for overseas tangible belongings | 8% incrementally diminished to five% over the primary 5 years |

| Exclusion for a Regular Return on Payroll Prices | No | No | No | No | 10% incrementally diminished to five% over the primary 5 years |

| Loss Carryovers | No | No | Capped at 80% of adjusted monetary assertion revenue and restricted to losses accrued after 2019 | No | Included in Deferred Tax Asset recast at 15% charge |

| Overseas Tax Therapy | Credit score for 80% of overseas taxes paid, no carryover for extra credit | Credit score for 80% of overseas taxes paid, no carryover for extra credit | Supplies a credit score for overseas taxes | Credit score for 95% of overseas taxes paid, five-year carryforward of extra overseas tax credit | Deferred Tax Asset recast at 15% charge |

| Jurisdictional Calculation | Overseas revenue is mixed collectively | Overseas revenue is mixed collectively | Applies to the worldwide revenue of U.S. corporations and the U.S. revenue of overseas corporations | Nation-by-country | Nation-by-country |

| Threshold for Utility | None, 10 % possession threshold | None, 10 % possession threshold | $1 billion in monetary income | None, 10 % possession threshold | €750 million ($790 million) in international revenues |

| Earnings Definition | Overseas taxable revenue as outlined within the Inner Income Code, no use of economic accounting strategies | Overseas taxable revenue as outlined within the Inner Income Code, no use of economic accounting strategies | Monetary income as outlined by accounting requirements and adjusted to align nearer to taxable income | Overseas taxable revenue as outlined within the Inner Income Code, no use of economic accounting strategies | Monetary income as outlined by accounting requirements and adjusted to align nearer to taxable income |

| Beneath-Taxed Income Rule (UTPR) | Base Erosion and Anti-Abuse Tax (not similar to the OECD mannequin guidelines) | Base Erosion and Anti-Abuse Tax (not similar to the OECD mannequin guidelines) | Base Erosion and Anti-Abuse Tax (not similar to the OECD mannequin guidelines) | Base Erosion and Anti-Abuse Tax (not similar to the OECD mannequin guidelines) | Sure |

| Certified Home Minimal High-Up Tax | None | None | Applies to home revenue, however it’s essentially completely different from a QDMTT | 15% different minimal tax on worldwide monetary income (not similar to the OECD mannequin guidelines) | Sure |

|

Supply: Writer’s evaluation of the worldwide guidelines within the Tax Cuts and Jobs Act, the Inflation Discount Act, and the worldwide minimal tax mannequin guidelines. |

|||||

The Pillar Two Guidelines and the U.S. Tax Base

Beneath the mannequin guidelines for the worldwide minimal tax, the taxable revenue of a giant multinational might be taxed by 5 layers of guidelines with every consecutive layer relying on how a lot tax is collected beneath the earlier one:

- Regular company revenue taxes within the jurisdiction wherein revenue is earned

- Certified Home Minimal High-Up Tax (QDMTT) utilized by the jurisdiction wherein low-tax earnings come up

- Managed Overseas Company (CFC) guidelines utilized by the jurisdiction of an organization’s headquarters or house owners

- Earnings Inclusion Rule (IIR) utilized by the jurisdiction of an organization’s final guardian entity on low-tax overseas earnings in every overseas jurisdiction wherein the corporate has low-tax earnings

- Beneath-Taxed Income Rule (UTPR) utilized to entities inside a jurisdiction on a rustic’s share of low-tax income of the company group that haven’t already been taxed by one of many earlier 4 guidelines

The U.S. at present has guidelines in place for numbers one and three. The U.S. company revenue tax applies on the federal stage with a 21 % charge, although numerous deductions and credit can lead to efficient tax charges under 21 %. The U.S. additionally has CFC guidelines that apply to the overseas revenue of U.S. multinationals in sure circumstances (Subpart F). GILTI additionally roughly matches into the CFC guidelines class. Credit for overseas taxes paid will be utilized to scale back extra U.S. tax legal responsibility, though they’re restricted to 80 % of their worth for GILTI, and up to date regulatory modifications have narrowed the scope of creditable overseas taxes.

The order of the minimal tax guidelines implies that each the U.S. tax base by Subpart F and thru GILTI might be eroded when different nations undertake a QDMTT. It’s because overseas tax credit for QDMTTs would offset the taxes that will in any other case be owed by Subpart F and GILTI. The 80 % overseas tax credit score restrict in GILTI implies that after a QDMTT applies, any income raised by GILTI is double taxation of overseas income.

The U.S. can be giving up the tax base it at present taxes utilizing GILTI. In truth, the worldwide minimal tax guidelines incentivize nations to undertake QDMTTs that will apply forward of IIRs and CFC guidelines. Analysis by economists Michael Devereux, John Vella, and Heydon Wardell-Burrus suggests some jurisdictions could desire to gather company taxes by the QDMTT than even the normal company tax.[32]

Tax Basis modeling from 2021 means that if sufficient overseas jurisdictions alter their company revenue taxes to gather low-tax earnings inside their jurisdictions, then aligning GILTI with the worldwide minimal tax would end in a internet lack of U.S. federal tax income.[33]

Except U.S. cross-border guidelines change, corporations will face GILTI, BEAT, and the brand new e-book minimal tax from the Inflation Discount Act along with compliance prices related to the worldwide minimal tax. It is a larger stage of coverage complexity and compliance than the overseas competitors U.S. corporations will face, and Congress ought to intention to keep away from a chaotic enforcement and compliance situation within the coming years.

The uncertainty within the present surroundings is pushed by the minimal tax guidelines and their interplay with U.S. guidelines. Along with interactions with GILTI and Subpart F, U.S. tax incentives have essential interactions with the worldwide minimal tax guidelines as nicely.

U.S. tax credit supplied to corporations for clear power initiatives, analysis and growth, or deductions linked to FDII can lead to low efficient tax charges, exposing the revenue of a overseas firm working within the U.S. to an IIR. The identical will be true for U.S. corporations that is likely to be uncovered to a UTPR on their low-tax revenue inside the U.S.[34]

Tax Incentives and the World Minimal Tax

Many jurisdictions around the globe supply tax preferences or construction their tax guidelines in such a method that permits corporations to be taxed at charges under the 15 % charge envisioned by the minimal tax.

The worldwide minimal tax can create issues for such insurance policies, nonetheless. For instance, let’s say a big multinational firm headquartered in Nation A makes an funding in Nation B that’s eligible for a 10-year company tax vacation. Despite the fact that the income from the funding is not going to be taxed by Nation B, the worldwide minimal tax would permit Nation A to use the minimal charge of 15 % to these income.

Nation B could select to alter its tax vacation coverage to tax these income domestically relatively than permitting the tax income to go to Nation A. If Nation B applies a excessive company tax charge to corporations that aren’t eligible for a tax vacation, the extra income from shutting down the preferential coverage might help a extra common tax reform (broadening the bottom and reducing the charges, because the mantra goes).

Not all tax insurance policies will observe such an easy evaluation, nonetheless, and the mannequin guidelines are solely useful in assessing insurance policies to the extent that they end in efficient tax charges under 15 % for big multinational corporations.

On the threat of oversimplifying, I’ve developed a tough categorization of the insurance policies that nations will more than likely have to assessment within the context of the minimal tax guidelines. That is proven in Determine 3. Insurance policies dealing with a Pink Mild are primarily people who present a zero efficient tax charge. Yellow Mild insurance policies present diminished efficient tax charges under 15 % however not zero. Inexperienced Mild insurance policies are people who cut back the price of funding with out triggering the minimal tax, until the overall company tax charge could be very low.

The important thing gadgets for U.S. lawmakers are within the Yellow Mild class. The FDII deduction and non-refundable credit each create a threat of a top-up tax by the worldwide minimal tax guidelines.

FDII is probably weak to top-up tax attributable to its 13.125 % charge. Decrease charges for intangible revenue are comparatively widespread worldwide; an OECD survey of 49 nations finds 27 have an income-based R&D incentive much like FDII. The FDII regime is among the many bigger income-based incentives as a share of its nation’s financial system, although far wanting the best outliers. In absolute phrases, it’s the largest on the earth. The administration’s efforts to repeal FDII led the OECD to categorize it as “within the means of being eradicated.” Nonetheless, Congress has not but agreed on laws to remove FDII, and its standing each domestically and with the OECD stays unsure.

As a result of reliance on accounting requirements for the worldwide minimal tax guidelines, non-refundable tax credit are handled worse than refundable credit. Nonetheless, it isn’t a easy matter to alter non-refundable credit into refundable credit. Latest evaluation by PwC suggests that reworking each FDII and common enterprise credit into refundable applications might lower U.S. tax income by as much as practically $200 billion over the 2023-2032 funds window.[37] That is earlier than accounting for behavioral modifications in response to the supply of refundability.

Uncertainty surrounding the long run compatibility of U.S. cross-border tax guidelines and tax incentives with the worldwide minimal tax straight undermines the TCJA insurance policies meant to help the success of multinationals linked to the U.S. market.

Designing a Strategic Method for U.S. Reforms

Despite the fact that Treasury has not sufficiently coordinated its worldwide negotiations with Congress, it is going to be Congress’ accountability to attenuate the disruption brought on by the implementation of the worldwide minimal tax.

Three targets ought to information lawmakers:

- Simplify the taxation of U.S. multinationals

- Promote funding and innovation within the U.S. in ways in which shield the U.S. tax base from overseas top-up taxes

- Goal for income impartial reforms

First, relating to simplicity, the overseas tax credit score is a crucial place to begin. The overseas tax credit score connections between GILTI in present legislation and the worldwide minimal tax contribute considerably to extra complexity for U.S. multinationals. And lately, the U.S. Treasury has promulgated rules which have added much more uncertainty across the overseas tax credit score.[38]

The present U.S. system is a hybrid system with components that solely deal with actions straight linked to the U.S. and components that have a look at an organization’s international footprint. Different nations which have had territorial methods for a few years are actually venturing out on this hybrid strategy with the worldwide minimal tax. The multinationals that face the minimal tax guidelines will primarily be working beneath a algorithm that apply to their worldwide revenue.

The tensions between territorial and worldwide guidelines will create complexity and enforcement challenges for years to come back.

Returning to a set of worldwide guidelines for U.S. corporations might be seen as a simplification relative to the complexities of administering a hybrid system and implementing the worldwide minimal tax guidelines.

Changing our present guidelines with a worldwide tax system with full creditability for overseas taxes might show less complicated for compliance than a reform that tries to align GILTI, BEAT, and the e-book minimal tax to the worldwide minimal tax guidelines. This might be accomplished alongside everlasting, growth-oriented reforms like returning to expensing for R&D and capital investments.

In 2020, I advisable {that a} international minimal tax must be designed with full expensing for capital expenditures.[39] The minimal tax guidelines typically don’t stand in the way in which of this coverage, so a worldwide tax base that features full expensing alongside a aggressive charge might be a worthwhile effort.

If policymakers select to not go down the trail of worldwide taxation and as an alternative retain a hybrid territorial system, it is going to be essential to undertake guidelines which might be on the very least suitable with the worldwide minimal tax guidelines. Having corporations calculate taxable revenue beneath probably 4 completely different minimal tax regimes can be counterproductive.

Secondly, Congress ought to promote funding and innovation within the U.S. in ways in which shield the U.S. tax base from overseas top-up taxes. To keep away from U.S. corporations shedding tax advantages to overseas UTPRs or overseas corporations working within the U.S. to IIRs, Congress ought to assessment current tax incentives and prioritize them for reform or elimination. Extra revenues from eradicated tax incentives might be used to increase investment-friendly insurance policies which might be extra suitable with the worldwide minimal tax, akin to full expensing for capital funding.[40]

The U.S. also needs to keep a comparatively low company tax charge in line with the worldwide settlement.

Lastly, coverage reforms ought to intention for income neutrality. Within the space of cross-border taxation, the construction and complexity of the principles matter tremendously. However as soon as the construction is about, policymakers ought to keep away from creating pointless tax will increase for companies. The TCJA needed to commerce off income reductions in some areas with base broadening, and the identical will probably be obligatory within the subsequent spherical of modifications to cross-border tax guidelines.

The selection for Congress just isn’t a easy one between adopting the worldwide minimal tax guidelines or adopting the reforms to GILTI envisioned within the BBBA. Total, taking a unique strategy would supply Congress an opportunity to simplify cross-border tax guidelines in a method that helps funding inside the U.S. with out giving up important management of the U.S. tax base to overseas jurisdictions.

Conclusion

Loads has modified in worldwide tax guidelines during the last decade. Congress ought to discover how new guidelines have impacted the U.S. tax base and the funding habits of U.S. corporations.

The present stage of uncertainty undermines the targets of the 2017 reforms. Coverage modifications that transfer the U.S. guidelines out of the fog and into longer-term stability can be welcome.

The U.S. worldwide tax system can and must be simplified. Such an achievement would require legislators to focus their efforts on designing guidelines that match inside the new framework and don’t unnecessarily quit management of the U.S. tax base.

Even within the face of a world minimal tax, Congress nonetheless has an opportunity to develop a strategic strategy in help of U.S. funding and innovation. It ought to take that probability.

[1] OECD/G20 Base Erosion and Revenue Shifting Venture, “Assertion on a Two-Pillar Answer to Handle the Tax Challenges Arising from the Digitalisation of the Financial system,” OECD, Jul. 1, 2021, https://www.oecd.org/tax/beps/statement-on-a-two-pillar-solution-to-address-the-tax-challenges-arising-from-the-digitalisation-of-the-economy-july-2021.pdf.

[2] Mindy Herzfeld, “A Pillar 2 Tour Across the World,” Tax Notes As we speak Federal, Apr. 17, 2023. https://www.taxnotes.com/tax-notes-today-federal/transfer-pricing/pillar-2-tour-around-world/2023/04/17/7ggwf.

[3] Tax Basis, “What Is Worldwide Tax System?,” accessed Might 2, 2023, https://taxfoundation.org/tax-basics/worldwide-taxation/.

[4] Cristina Enache, “Company Tax Charges Across the World,” Tax Basis, Dec. 13, 2022, https://taxfoundation.org/publications/corporate-tax-rates-around-the-world/.

[5] Tax Basis, “What Is Territorial Tax System?,” accessed Might 2, 2023, https://taxfoundation.org/tax-basics/territorial-taxation/.

[6] Bureau of Financial Evaluation, “Desk 4.2. U.S. Worldwide Transactions in Main Earnings on Direct Funding, Receipts, Dividends and Withdrawals,” Mar. 23, 2022.

[7] Brooke Beyer et al., “Early Proof on the Use of Overseas Money Following the Tax Cuts and Jobs Act of 2017,” Social Science Analysis Community, Apr. 2, 2021, https://doi.org/10.2139/ssrn.3818149.

[8] Garrett Watson et al., “Canceling the Scheduled Enterprise Tax Will increase in Tax Cuts and Jobs Act,” Tax Basis, Nov. 1, 2022, https://taxfoundation.org/tax-cuts-jobs-act-business-tax-increases/.

[9] John McClelland and Jeffrey Werling, “How the 2017 Tax Act Impacts CBO’s Projections,” Congressional Finances Workplace, Apr. 20, 2018, https://www.cbo.gov/publication/53787; Huaqun Li and Kyle Pomerleau, “The Distributional Influence of the Tax Cuts and Jobs Act over the Subsequent Decade,” Tax Basis, Jun. 28, 2018, https://taxfoundation.org/the-distributional-impact-of-the-tax-cuts-and-jobs-act-over-the-next-decade/.

[10] Thornton Matheson et al., “The Influence of the Tax Cuts and Jobs Act on Overseas Funding in the US.” IMF Working Papers 22/79, Might 2022, https://www.imf.org/en/Publications/WP/Points/2022/05/06/The-Influence-of-the-Tax-Cuts-and-Jobs-Act-on-Overseas-Funding-in-the-United-States-517616.

[11] For extra data on the mechanics of those insurance policies, see Kyle Pomerleau, “A Hybrid Method: The Therapy of Overseas Income beneath the Tax Cuts and Jobs Act,” Tax Basis, Might 2018, https://recordsdata.taxfoundation.org/20180502205047/Tax-Basis-FF586.pdf.

[12] Tax Basis, “World Intangible Low Tax Earnings (GILTI),” accessed Might 2, 2023. https://taxfoundation.org/tax-basics/global-intangible-low-tax-income-gilti/.

[13] Cody Kallen, “How Closely Taxed Are U.S. Multinationals?,” Tax Basis, Sep. 29, 2021, https://www.taxfoundation.org/us-multinational-corporations-tax/.

[14] Mathias Dunker, Michael Overesch, and Max Pflitsch, “The Results of the U.S. Tax Reform on Investments in Low-Tax Jurisdictions – Proof from Cross-Border M&As,” Social Science Analysis Community, Sep. 28, 2021, https://doi.org/10.2139/ssrn.3932459.

[15] Harald Amberger and Leslie A. Robinson, “The Preliminary Impact of U.S. Tax Reform on Overseas Acquisitions,” Social Science Analysis Community, Feb. 6, 2023, https://doi.org/10.2139/ssrn.3612783.

[16] “What Is the Certified Enterprise Asset Funding (QBAI) Exemption?,” Tax Basis, accessed Might 2, 2023, https://taxfoundation.org/tax-basics/qualified-business-asset-investment-qbai-exemption/.

[17] Beyer et al., “Early Proof on the Use of Overseas Money Following the Tax Cuts and Jobs Act of 2017.”

[18] Martin A. Sullivan, “Newest SEC Filings Present FDII Advantages Proceed to Climb,” Tax Notes As we speak Worldwide, Apr. 10, 2023, https://www.taxnotes.com/tax-notes-today-international/corporate-taxation/latest-sec-filings-show-fdii-benefits-continue-climb/2023/04/10/7g9qj.

[19] Javier Garcia-Bernardo, Petr Janský, and Gabriel Zucman, “Did the Tax Cuts and Jobs Act Cut back Revenue Shifting by US Multinational Corporations?,” Nationwide Bureau of Financial Analysis, Might 2022, https://www.nber.org/papers/w30086.

[20] Daniel Bunn, “New Analysis Reveals Main Modifications for U.S. Corporations Incomes Income from Eire,” Tax Basis, Jun. 16, 2021, https://taxfoundation.org/us-companies-earning-profits-ireland/.

[21] Ibid.

[22] Seamus Coffey, “The altering nature of outbound royalties from Eire and their impression on the taxation of the income of US multinationals – Might 2021,” Eire Division of Finance, Jun. 14, 2021, https://www.gov.ie/en/publication/fbe28-the-changing-nature-of-outbound-royalties-from-ireland-and-their-impact-on-the-taxation-of-the-profits-of-us-multinationals-may-2021/.

[23] The BEAT charge is scheduled to rise to 12.5 % starting in 2026. The $500 million in revenues is measured as a three-year transferring common. The BEAT charge of 10 % applies to a U.S. firm’s taxable revenue plus the worth of base erosion funds minus legal responsibility for regular company tax. For an instance of a BEAT calculation, see Kyle Pomerleau, “A Hybrid Method: The Therapy of Overseas Income beneath the Tax Cuts and Jobs Act.”

[24] “Common Explanations of the Administration’s Fiscal Yr 2024 Income Proposals” Division of the Treasury, Mar. 9, 2023, https://house.treasury.gov/system/recordsdata/131/Common-Explanations-FY2024.pdf.

[25] Scott Dyreng et al., “The Impact of U.S. Tax Reform on the Tax Burdens of U.S. Home and Multinational Companies,” Social Science Analysis Community, Jun. 5, 2020, https://doi.org/10.2139/ssrn.3620102.

[26] “Monitoring Tax Runaways,” Bloomberg.Com, Apr. 13, 2023, https://www.bloomberg.com/graphics/tax-inversion-tracker/.

[27] Mindy Herzfeld, “Designing Worldwide Tax Reform: Classes from TCJA,” Worldwide Tax and Public Finance 28: 5 (2021): 1163–87, https://doi.org/10.1007/s10797-021-09675-0.

[28] The Biden administration has proposed to repeal FDII and change it with unspecified analysis and growth incentives, see “Common Explanations of the Administration’s Fiscal Yr 2024 Income Proposals” Division of the Treasury, Mar. 9, 2023, https://house.treasury.gov/system/recordsdata/131/Common-Explanations-FY2024.pdf.

[29] OECD, “Tax Challenges Arising from the Digitalisation of the Financial system – World Anti-Base Erosion Mannequin Guidelines (Pillar Two),” Dec. 20, 2021, https://www.oecd.org/tax/beps/tax-challenges-arising-from-the-digitalisation-of-the-economy-global-anti-base-erosion-model-rules-pillar-two.htm.

[30] See “OECD Releases Detailed Technical Steering on the Pillar Two Mannequin Guidelines for 15% World Minimal Tax – OECD,” accessed Might 2, 2023, https://www.oecd.org/tax/beps/oecd-releases-detailed-technical-guidance-on-the-pillar-two-model-rules-for-15-percent-global-minimum-tax.htm; “Worldwide Tax Reform: OECD Releases Technical Steering for Implementation of the World Minimal Tax – OECD,” accessed Might 2, 2023, https://www.oecd.org/tax/international-tax-reform-oecd-releases-technical-guidance-for-implementation-of-the-global-minimum-tax.htm.

[31] No such exclusion thresholds can be found for U.S. corporations beneath GILTI (present legislation or within the BBBA).

[32] Michael P. Devereux, John Vella, and Heydon Wardell-Burrus, “Pillar 2: Rule Order, Incentives, and Tax Competitors,” Oxford College Centre for Enterprise Taxation Coverage Temporary, Jan. 14, 2022, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4009002.

[33] See the second desk in Daniel Bunn, “Adoption of World Minimal Tax May Elevate U.S. Income…or Not,” Tax Basis, Aug. 19, 2021, https://www.taxfoundation.org/us-global-minimum-tax-revenue/.

[34] Daniel Bunn, “U.S. Tax Incentives Could possibly be Caught within the World Minimal Tax Crossfire,” Tax Basis, Jan. 28, 2022, https://www.taxfoundation.org/us-global-minimum-tax-build-back-better/.

[35] Silvia Appelt et al., “Value and uptake of income-based tax incentives for R&D and innovation,” OECD Science, Know-how and Trade Working Papers, https://www.oecd-ilibrary.org/docserver/4f531faf-en.pdf.

[36] OECD, “Dangerous Tax Practices – Peer Evaluation Outcomes,” Inclusive Framework on BEPS: Motion 5, January 2023, https://www.oecd.org/tax/beps/harmful-tax-practices-consolidated-peer-review-results-on-preferential-regimes.pdf.

[37] Peter R. Merrill et al., “The place Credit score Is Due: Therapy of Tax Credit Beneath Pillar 2,” accessed Might 2, 2023, https://www.taxnotes.com/special-reports/credit/where-credit-due-treatment-tax-credits-under-pillar-2/2023/03/17/7g743#sec-4-1-1. If solely utilized to corporations with gross revenues >=€750 million, the price might be considerably decrease.

[38] Daniel Bunn, “A regulatory tax hike on US multinationals,” MNE Tax, Feb. 28, 2022, https://mnetax.com/a-regulatory-tax-hike-on-us-multinationals-46865.

[39] Daniel Bunn, “Designing a World Minimal Tax with Full Expensing,” Tax Basis, Sep. 23, 2020, https://taxfoundation.org/designing-a-global-minimum-tax-with-full-expensing/.

[40] For extra evaluation of the connection between the worldwide minimal tax and tax incentives, see Desk III.2 in UNCTAD, “World Funding Report 2022,” June 2022, https://unctad.org/system/recordsdata/official-document/wir2022_en.pdf.

/a-7-5bfc2b3c4cedfd0026c10a26.jpg)