Georgina Inexperienced

The take-up of mortgage cost holidays within the UK through the Covid-19 pandemic was extraordinary: based on UK Finance, holidays granted reached a peak of 1.9 million through the pandemic, or roughly one in six mortgages. However which households benefited from the scheme? On this publish I exploit wealthy UK family survey knowledge to conduct an in-depth evaluation of the distribution of the debt-relief scheme at a person stage. I discover that debtors struggling to maintain up with funds throughout Covid utilized for a vacation, suggesting the scheme performed an vital function in stopping a pointy rise in defaults. There’s additionally proof that some households might have taken them as insurance coverage in opposition to future shocks, probably dampening precautionary spending cuts.

What are cost holidays?

The unfold of Covid and the actions to include it had a major impression on UK family incomes and had the potential to trigger a major rise in family debt misery. Nonetheless, from March 2020 cost deferral schemes, often called ‘cost holidays’, had been shortly rolled-out throughout the UK. They supplied a type of forbearance to debtors struggling due to Covid, by permitting a brief freeze on mortgage repayments.

The schemes had been provided by lenders for as much as six months following steerage from the UK conduct regulator, the Monetary Conduct Authority. Mortgagors had been eligible so long as they weren’t already behind on funds and debtors had been informed that holidays wouldn’t be reported as missed funds on their credit score file, impacting their credit score scores.

As most mortgagors had been eligible for a vacation, understanding which households utilized for the schemes is of key significance for coverage. Of explicit curiosity, is whether or not deferrals went to households whose funds had come underneath pressure on account of the pandemic, resembling: these whose well being was affected and had been quickly unable to work due to this; these shielding due to underlying well being vulnerabilities; and those that misplaced revenue on account of lockdowns, resembling those that had been furloughed or unemployed. The results of cost deferrals going to households in want are extremely materials. By making certain households stayed present on their mortgages, the schemes might have prevented a pointy rise in defaults and spending cuts, which may have had unfavorable spillovers to the remainder of the financial system. Certainly, all through the pandemic mortgage arrears remained close to to traditionally low ranges. And although family spending fell considerably, largely pushed by curbs on social exercise, it could have declined even additional had cost deferrals not been launched to assist households.

Use of family survey knowledge to look at who accessed mortgage cost holidays within the UK

I exploit granular knowledge protecting round 3,000 UK mortgagors collected from the Understanding Society Covid-19 Research. Understanding Society is the UK’s primary longitudinal family survey. The Covid research was launched to seize experiences of a subset of those households through the pandemic.

The primary time a family was interviewed they had been requested if that they had utilized for a mortgage cost vacation. I pool collectively all of the responses to this query throughout three waves (in April, Could and July 2020) to create my pattern. In my pattern, 12% of mortgagors responded that that they had utilized for a cost vacation. Of those functions, round 1% had been nonetheless underneath overview with solely 0.1% having been declined. That only a few functions had been declined confirms that cost holidays had been largely pushed by borrower demand reasonably than lender provide. The functions underneath overview on the time of the survey had been probably delayed by capability constraints amongst lenders. I subsequently concentrate on all functions reasonably than solely these granted to maximise my pattern measurement.

To discover predictors of responses to the cost deferral query I hyperlink info from the Covid surveys (age; ethnicity; revenue; well being; employment; and monetary issues) to vital pre-crisis family traits from the primary survey, resembling mortgage debt, web financial savings and former housing cost difficulties.

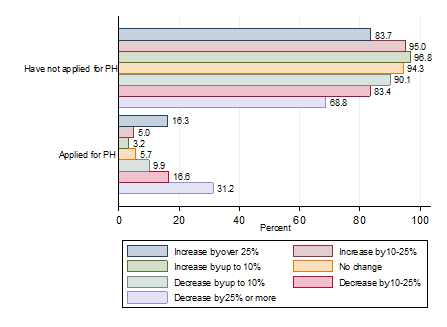

I discover that variables which point out that a person’s funds had come underneath pressure through the pandemic are correlated with choices to use. When nothing else is managed for, households which had skilled a fall in earnings had been extra more likely to apply for a vacation than others, notably if the autumn exceeded 25% (Chart 1). Whereas it’s shocking {that a} comparatively giant share of households which skilled rises in earnings of over 25% nonetheless utilized for deferrals, these households tended to be a lot worse-off previous to the pandemic. On common, pre-Covid family earnings for this group had been 45% decrease than different households that utilized for deferrals. Because of this, even regardless of the rise in revenue, they could have been struggling financially. People who anticipated to be worse off within the following month had been additionally significantly extra more likely to apply for a deferral, suggesting precautionary causes might have been vital (Chart 2).

Chart 1: Cost deferral by change in family web earnings between January/February 2020 and the interview date (per cent)

Sources: Understanding Society Covid-19 Research and Financial institution calculations.

Chart 2: Cost deferral by monetary expectations one month forward (per cent)

Sources: Understanding Society Covid-19 Research and Financial institution calculations.

Did cost deferrals go to individuals whose funds had come underneath pressure on account of the pandemic?

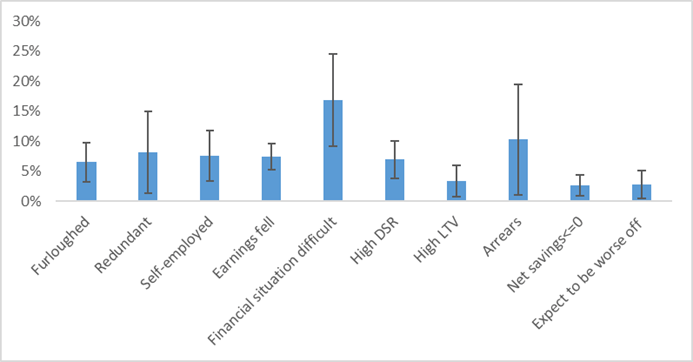

To formally examine which traits are related to functions for cost holidays I run logit regressions, which mannequin the chance of an occasion occurring. My baseline outcomes are proven in Chart 3. I report the marginal results, which inform us the impression of a variable on the chance of making use of for a cost vacation, holding all different variables at their common stage.

I discover proof that many deferrals went to these whose funds had come underneath pressure. Being furloughed, dropping family earnings or being made redundant for the reason that begin of the pandemic are all economically and statistically important predictors of deferral functions. People who’re self-employed are additionally considerably extra more likely to have utilized for a deferral than the typical. That is consistent with proof that the self-employed had been notably arduous hit by the pandemic and restrictions to include it. Essentially the most economically important predictor is a person’s subjective present monetary state of affairs: those that had been discovering their current monetary state of affairs tough, had been round 17% extra more likely to apply for a deferral.

No well being variables – resembling having had signs of Covid up to now or having examined constructive for Covid – are important. It’s probably that the strain on family funds from being sick with Covid and having to self-isolate is already being soaked up by the revenue and job standing variables.

Chart 3: Outcomes logit regression

Notes: Error bars characterize 90% confidence intervals round imply marginal results. ‘Earnings fall’ refers back to the change in family web earnings between January/February 2020 and the person’s first-response to the Covid survey. ‘Internet financial savings’ is calculated as family financial savings web of complete shopper credit score. ‘Excessive DSR’ is a binary variable indicating whether or not a family’s mortgage debt servicing ratio was within the prime quintile. ‘Excessive LTV’ signifies whether or not a family’s mortgage mortgage to worth ratio was within the prime quintile. Further variables managed for in regression however not proven embrace: capability to work at home; results of Covid take a look at; had signs of Covid; mortgage mortgage to revenue ratio; family web revenue; NHS informed to ‘protect’; age; kids; gender; marital standing; and ethnicity.

Who else took cost holidays?

My outcomes additionally counsel the coverage inspired financially weak households, who had not suffered any sort of Covid-related shock to their funds, to use.

Mortgagors with a excessive debt-servicing ratio, excessive mortgage to worth ratio, unfavorable family web financial savings or those that had beforehand been in arrears, had been extra more likely to apply even when adjustments in revenue and job standing are managed for. These people probably confronted borrowing and liquidity constraints and should have used the schemes to construct up a buffer of financial savings to insure in opposition to future shocks. Expectations additionally appear to matter. People who anticipated to be financially worse off in a single months’ time additionally had a statistically considerably greater predicted chance of making use of.

These outcomes are sturdy to quite a lot of assessments, together with controlling for the month of interview, area, the removing of weights and adjustments within the pattern.

Conclusions

Total, my outcomes counsel that many deferrals flowed to these whose funds had come underneath pressure on account of the pandemic. Certainly, a family’s subjective monetary state of affairs being tough is the strongest predictor of making use of for cost deferrals. It’s subsequently potential that deferrals helped forestall an increase in defaults and dampened family spending cuts. However expectations and pre-Covid balance-sheet variables mattered too, even when employment and revenue are managed for. This suggests that some functions may have been made for precautionary causes. Due to this fact the schemes might have dampened spillovers to the true financial system even additional by stopping financially weak and pessimistic mortgagors from chopping again on their spending.

Georgina Inexperienced works within the Financial institution’s Macro-financial Dangers Division.

If you wish to get in contact, please e mail us at [email protected] or go away a remark beneath.

Feedback will solely seem as soon as authorized by a moderator, and are solely printed the place a full title is equipped. Financial institution Underground is a weblog for Financial institution of England workers to share views that problem – or assist – prevailing coverage orthodoxies. The views expressed listed here are these of the authors, and should not essentially these of the Financial institution of England, or its coverage committees.

/a-7-5bfc2b3c4cedfd0026c10a26.jpg)