The Tax Cuts and Jobs Act (TCJA) of 2017 made a number of modifications to the U.S. tax system to boost competitiveness and discourage revenue shifting to low-tax jurisdictions by U.S. multinationals. Amongst them have been a brand new 10 p.c minimal tax on corporations with important cross-border transactions (BEAT) and new tax charges on deemed intangible earnings (GILTI and FDII). International income paid to U.S. dad and mom as dividends have been absolutely exempt from U.S. taxation, shifting the U.S. tax system nearer to “territorial” tax therapy moderately than worldwide. Lastly, the highest marginal company tax fee was decreased from 35 p.c to 21 p.c.

Altogether, policymakers anticipated the modifications to considerably impression capital flows throughout borders. Collectively, the modifications would cut back incentives to spend money on low-tax jurisdictions, because the tax hole between these jurisdictions and better tax nations would shrink, and doubtlessly shift a few of this funding overseas to the U.S.

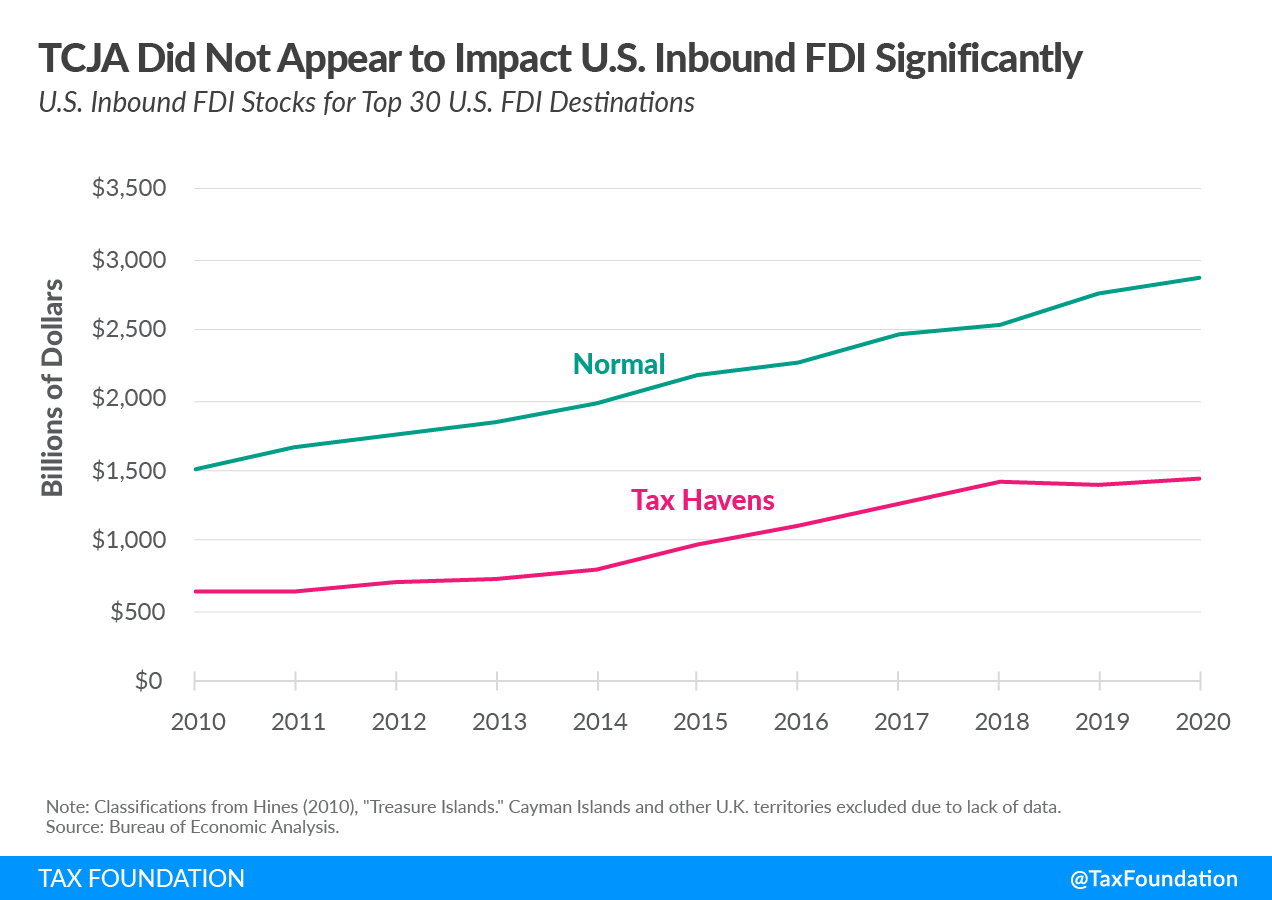

When taking a look at outbound overseas direct funding (FDI), funding that flows from the U.S. to different nations, we are able to see the TCJA seems to have had an impression on the place corporations are investing. The next chart exhibits developments in FDI shares for the highest 30 locations of U.S. FDI. Nations are labeled as “tax havens” based mostly on analysis of FDI shares achieved by economist James Hines.

Following the TCJA, outbound U.S. FDI shares fell by $192 billion within the tax havens and rose by $251 billion within the “regular,” or high-tax, nations. The “tax havens” group is comprised of 10 nations or territories, together with Eire, Bermuda, Switzerland, and the Cayman Islands. This pattern displays modifications to revenue shifting incentives following the TCJA, as analysis has discovered that companies affected by GILTI have been much less more likely to spend money on low-tax jurisdictions.

When taking a look at U.S. inbound FDI throughout the identical set of nations, funding that flows from overseas nations to the U.S., the TCJA doesn’t seem to have brought about a lot of a break within the developments. Inbound U.S. FDI continued to develop at an analogous tempo from high-tax jurisdictions, whereas inbound U.S. from the tax havens continued to develop however at a slower fee than it had from 2014 to 2018. Analysis has discovered the continued upward pattern in inbound FDI was extra probably attributable to macroeconomic elements apart from the TCJA.

General, the info exhibits outbound FDI shifted from low-tax to different jurisdictions, whereas inbound FDI remained largely unchanged. However as famous within the first and second of our FDI weblog publish collection, elevated overseas exercise needn’t essentially come on the expense of the U.S. workforce and manufacturing trade. U.S. funding in different nations usually generates advantages for the U.S. and helps strengthen provide chains, and policymakers ought to maintain this in thoughts when making an attempt to lift taxes on cross-border funding.

/a-7-5bfc2b3c4cedfd0026c10a26.jpg)