Company tax reforms launched by the 2017 Tax Cuts and Jobs Act (TCJA) inspired foreign-owned US firms to reinvest extra of their earnings right here, in line with a brand new TPC research. The research additionally finds a optimistic relationship between the TCJA tax cuts and foreign-owned firms’ funding in US tangible belongings.

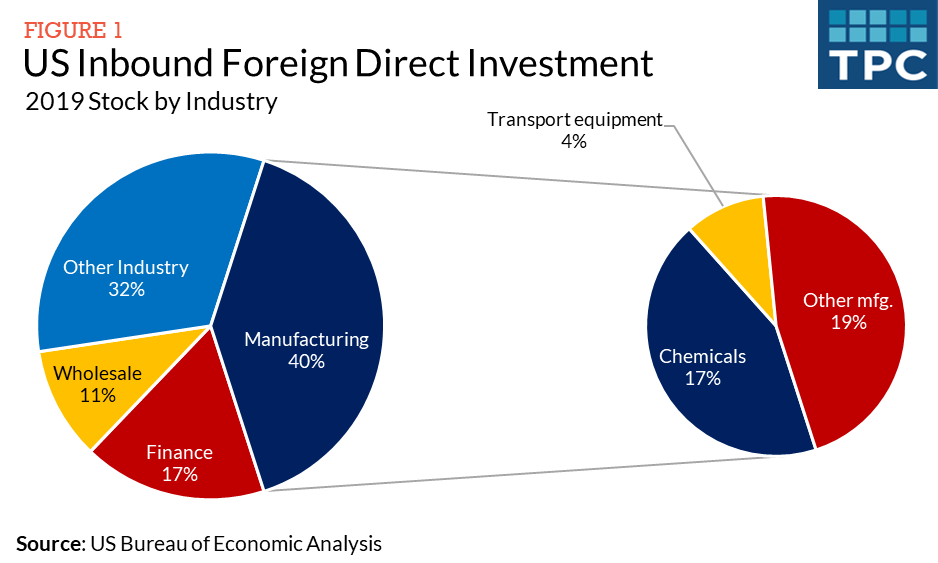

International funding accounts for about 15 p.c of US non-public enterprise capital funding, analysis and improvement spending, and company tax revenues. It’s closely concentrated in manufacturing, notably pharmaceutical chemical substances.

TPC evaluated two measures of international funding: Inbound international direct funding (FDI) measures monetary inflows from international buyers with minimal possession stakes in US firms, which will be financed with new fairness, loans, or retained earnings. Funding in property, plant, and tools (PPE) measures foreign-owned US firms’ funding in tangible belongings.

TCJA made sweeping modifications to the US company earnings tax that sharply lowered its general burden. TCJA minimize the US company tax charge from 35 to 21 p.c, and the international derived intangible earnings (FDII) regime decreased the tax charge on extra returns from exports to about 13 p.c. Short-term full expensing of most tools funding (“bonus depreciation”) additionally narrowed the company tax base. Conversely, TCJA broadened the tax base by limiting curiosity expense deductibility and introducing the bottom erosion anti-abuse tax (BEAT), which disallows some deductions to international associated events.

TPC’s research captured each charge and base modifications by specializing in efficient tax charges calculated utilizing its worldwide funding and capital mannequin (IICM).

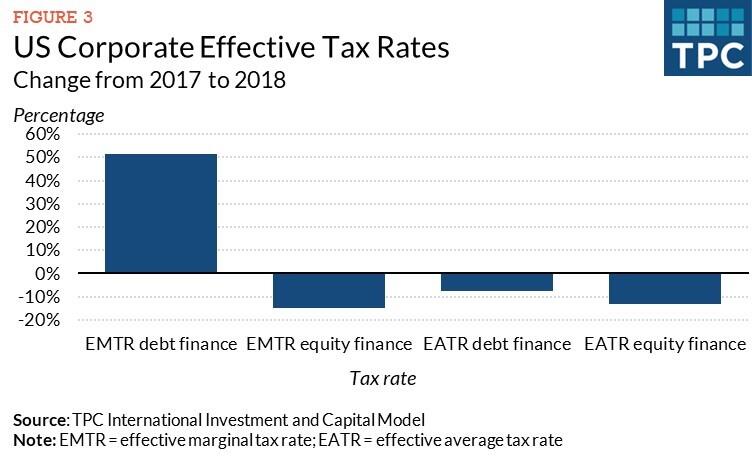

The efficient marginal tax charge (EMTR) measures the share of taxes within the gross return on an funding that simply breaks even after taxes. The EMTR on equity-financed funding fell from 28 p.c to 14 p.c in 2018. Nevertheless, the reform raised the unfavorable EMTR on debt-financed funding much more sharply, from about -80 p.c to -30 p.c.

The efficient common tax charge (EATR) is the ratio of the current worth of tax legal responsibility from a worthwhile funding to the current worth of its pretax earnings. The EATR is especially related to cross-border funding selections, the place corporations resolve amongst different jurisdictions the place to find a mission based mostly on general tax burden. For a mission incomes a 20 p.c charge of return, each debt and fairness EATRs fell by about one third in response to TCJA.

The IICM permits calculation of EMTRs and EATRs on the nation stage, differentiated by country-specific company and cross-border withholding taxes, and on the trade stage, differentiated by asset composition.

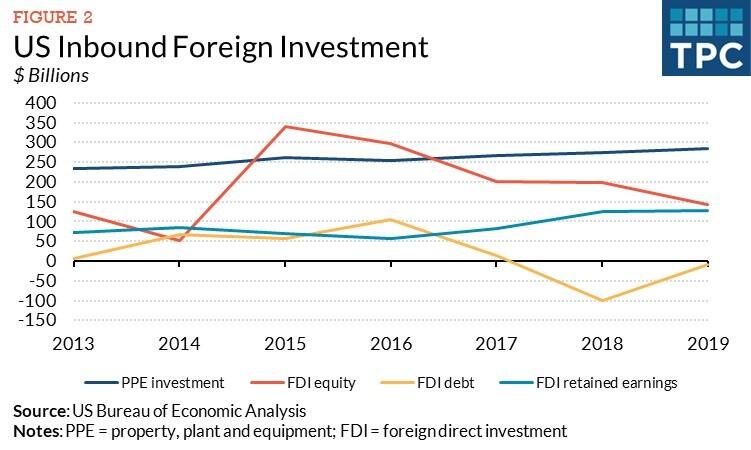

Estimates point out that FDI financed with retained earnings rose in response to the minimize in US EMTRs and EATRs, even when controlling for GDP development and greenback change charges. On common, retained earnings rose about 0.5 p.c in response to every percentage-point fall within the EMTR and three p.c in response to every one-point fall within the EATR. The funding response to the change in EATRs is just like that present in in different financial research.

Funding in PPE additionally rose following the TCJA tax minimize, however much less strongly. On common, about 0.35 p.c for every share level decline within the EMTR and 0.75 p.c for every share level decline within the EATR. Nevertheless, the connection between tangible funding and tax charges weakened when macroeconomic controls have been launched.

TCJA tax cuts thus seem to have spurred funding in tangible belongings primarily by way of their stimulative impact on combination demand. This discovering corroborates different early empirical research of TCJA by Invoice Gale and Claire Haldeman and the Worldwide Financial Fund.

TPC doesn’t discover proof that international direct funding (FDI) financed with new fairness or debt responded to the tax reform. Debt-financed FDI dropped sharply in 2018 however then rebounded the next yr. Since foreign-owned US firms additionally borrow in US capital markets, they could additional have adjusted their leverage by way of that channel.

Fairness-financed FDI, which is basically pushed by acquisitions of current US firms, fell following TCJA. TPC finds that the decline in equity-financed FDI was pushed by the increase and bust of “inversions”: transactions wherein a US company turns into a foreign-owned company, usually by way of merger or acquisition. These transactions, which generate an FDI influx to accumulate US inventory, peaked in 2015 after which declined resulting from tighter US Treasury rules in addition to the TCJA reform.

In sum, we discover TCJA’s massive discount in efficient tax charges induced international buyers to retain extra earnings within the US. Decrease company taxes additionally supported international funding in tangible belongings.

/a-7-5bfc2b3c4cedfd0026c10a26.jpg)